Introduction

In Chapters 1 and 2, we explored statistical approaches to synthetic data generation—sampling from distributions, estimating parameters from real data, and replicating statistical properties. These methods work exceptionally well when your goal is to preserve marginal distributions and basic correlations. But what happens when your data is deeply structured by business logic, physical laws, or complex interdependencies?

Consider a financial dataset of banking transactions. While statistical methods can generate transaction amounts that follow the right distribution, they cannot easily encode the rule that "gas station purchases are always between $20 and $150," or that "transfers only occur on business days," or that "fraud patterns cluster around certain merchant categories." Similarly, medical data has protocols: patients on certain medications must have specific lab values; diagnoses determine treatment eligibility.

This is where rule-based and simulation-driven approaches shine. Rather than learning patterns from data, we explicitly encode the logic that governs how data is generated. In this chapter, we explore six major methodologies that take us beyond pure statistics:

- Rule-based generators that produce plausible individual records via domain knowledge

- Template-based systems that parameterize structured documents

- Monte Carlo simulation for probabilistic estimation and modeling

- Agent-based models that simulate autonomous entities and emergent behavior

- Discrete event simulation for queue and process dynamics

- Physics-based simulation for sensor and robotic data

Beyond Statistics: Domain-Driven Generation

The fundamental insight underlying rule-based generation is this: real data is constrained by the system that creates it. A database schema doesn't just describe data; it encodes rules. A business process doesn't just produce random events; it follows workflows. A physical system doesn't generate observations arbitrarily; it follows physical laws.

There are several scenarios where rule-based generation is superior:

- Enforcement of hard constraints: "Customer age must be 18-120" is trivially enforced by rules but may require complex rejection sampling in statistical methods.

- Incorporating rare events: Fraud, system failures, or unusual scenarios can be explicitly injected with controlled frequency.

- Reproducible variation: Rules allow fine-grained control over data characteristics (e.g., "vary transaction amounts between 10% and 150% of category average").

- Documentation and auditability: Rules serve as executable documentation of data assumptions.

- Cross-domain consistency: Rules ensure that related entities remain consistent (e.g., a customer's ZIP code must match a valid address format).

The downside is that rule-based generation requires upfront domain knowledge and maintenance. As business logic evolves, your generators must be updated. And unlike statistical methods that adapt to changing data patterns automatically, rules are static until manually revised.

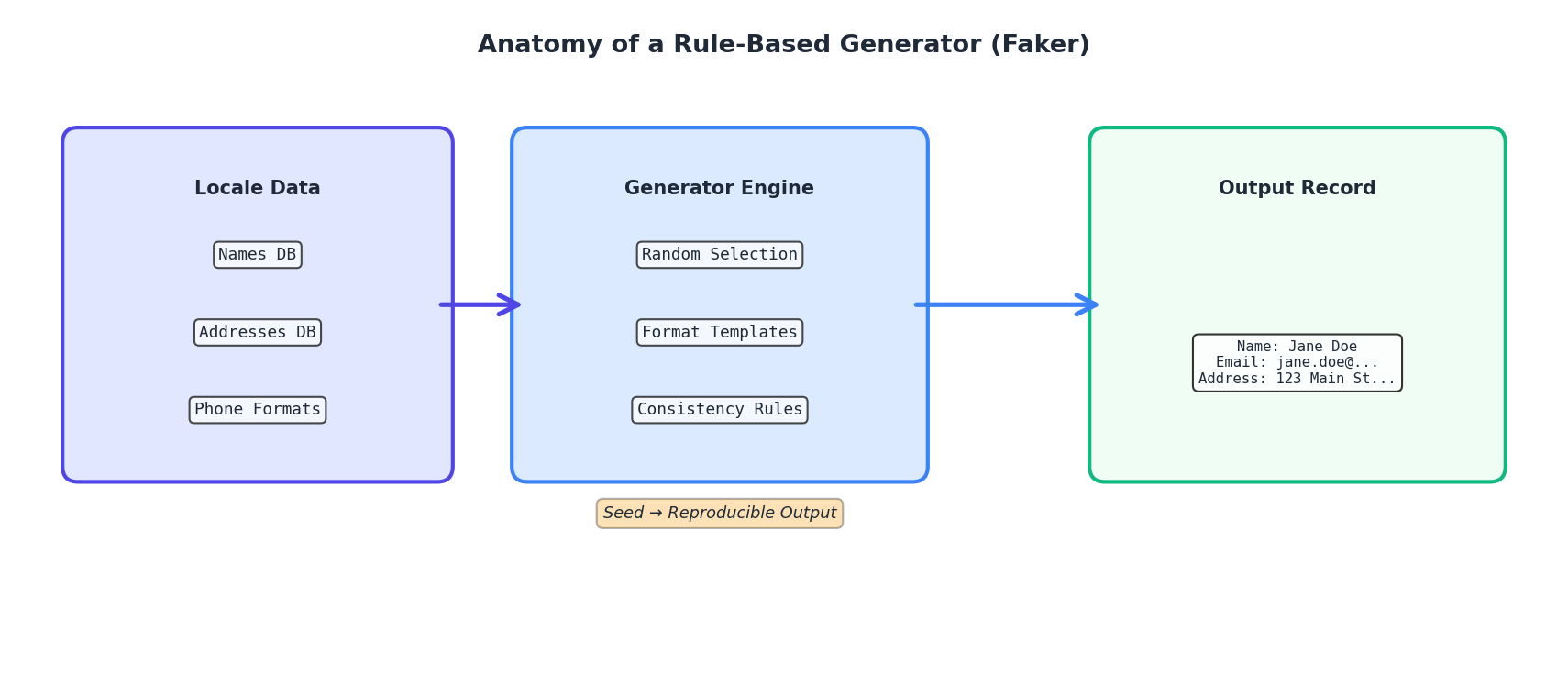

Rule-Based Generators: The Faker Library

The most practical tool for generating realistic individual records is the Faker library. Faker is a Python package that generates fake but plausible data: names, addresses, email addresses, phone numbers, dates, company names, and hundreds of other data types. Under the hood, Faker uses seed-based randomization combined with curated lists of real-world entries (e.g., authentic street names, actual company suffixes).

Let's start with a basic example:

from faker import Faker

fake = Faker()

# Generate a single fake person

for _ in range(5):

print(f"{fake.name()} | {fake.email()} | {fake.phone_number()}")

Output:

James Brown | james.brown@example.com | (212) 555-0123

Sarah Johnson | sarah.johnson@example.com | (718) 555-0456

Michael Chen | michael.chen@example.com | (646) 555-0789

Emily Rodriguez | emily.rodriguez@example.com | (917) 555-0234

David Patel | david.patel@example.com | (212) 555-0567

Faker is seed-aware, so for reproducibility:

Faker.seed(42)

fake = Faker()

# This will generate the same sequence every time

print(fake.name()) # Output: Anthony Garcia

print(fake.name()) # Output: Rebecca Lee

Now let's build a realistic customer dataset combining Faker with domain logic:

from faker import Faker

import random

import json

from datetime import datetime, timedelta

fake = Faker()

Faker.seed(42)

random.seed(42)

def generate_customers(n=100):

"""Generate n synthetic customers with realistic attributes."""

customers = []

# Define US states (simplified)

states = ['CA', 'NY', 'TX', 'FL', 'IL', 'PA', 'OH', 'GA', 'NC', 'MI']

for customer_id in range(1, n + 1):

# Name and contact

first_name = fake.first_name()

last_name = fake.last_name()

customer = {

'id': customer_id,

'name': f"{first_name} {last_name}",

'email': fake.email(),

'phone': fake.phone_number(),

# Address (using Faker)

'street': fake.street_address(),

'city': fake.city(),

'state': random.choice(states),

'zip': fake.postcode(),

# Account info

'account_created': (

datetime.now() - timedelta(days=random.randint(30, 1825))

).isoformat(),

'account_status': random.choices(

['active', 'inactive', 'suspended'],

weights=[0.85, 0.10, 0.05]

)[0],

# Spending profile

'annual_spend': round(random.gauss(5000, 2000), 2),

'account_tier': random.choices(

['bronze', 'silver', 'gold', 'platinum'],

weights=[0.50, 0.30, 0.15, 0.05]

)[0],

}

# Ensure spending is positive

customer['annual_spend'] = max(customer['annual_spend'], 0)

customers.append(customer)

return customers

# Generate and display sample

customers = generate_customers(5)

for c in customers:

print(json.dumps(c, indent=2))

For more complex scenarios, you can extend Faker with custom providers:

from faker import Faker

from faker.providers import BaseProvider

class TransactionProvider(BaseProvider):

"""Custom provider for transaction-related data."""

MERCHANT_CATEGORIES = [

'grocery', 'gas_station', 'restaurant', 'online_retail',

'utilities', 'healthcare', 'entertainment', 'travel'

]

def merchant_category(self):

return self.random.choice(self.MERCHANT_CATEGORIES)

def transaction_amount(self, category=None):

"""Generate realistic amount based on category."""

ranges = {

'grocery': (15, 150),

'gas_station': (20, 80),

'restaurant': (10, 200),

'online_retail': (5, 500),

'utilities': (50, 300),

'healthcare': (25, 1000),

'entertainment': (10, 100),

'travel': (50, 1000),

}

if category is None:

category = self.merchant_category()

min_amt, max_amt = ranges.get(category, (5, 500))

return round(self.random.uniform(min_amt, max_amt), 2)

fake = Faker()

fake.add_provider(TransactionProvider)

# Now use the custom provider

for _ in range(3):

cat = fake.merchant_category()

amt = fake.transaction_amount(cat)

print(f"{cat}: ${amt}")

Output:

gas_station: $45.23

online_retail: $234.56

grocery: $67.89

Template-Based Generation

Template-based generation takes rule-based methods a step further by defining parameterized structures. Instead of generating individual fields, you define a template—a structured document with placeholders—and then fill it with appropriate values.

A practical example is generating medical records. A medical record has a specific structure: patient demographics, vital signs, diagnoses, medications, lab results. Rather than generating each field independently, you can define a template that ensures these elements cohere logically.

import json

import random

from datetime import datetime, timedelta

from faker import Faker

fake = Faker()

class MedicalRecordTemplate:

"""Template for synthetic medical records with domain constraints."""

DIAGNOSES = {

'hypertension': {'icd10': 'I10', 'medications': ['lisinopril', 'metoprolol']},

'diabetes': {'icd10': 'E11', 'medications': ['metformin', 'glipizide']},

'asthma': {'icd10': 'J45', 'medications': ['albuterol', 'fluticasone']},

'copd': {'icd10': 'J44', 'medications': ['tiotropium', 'albuterol']},

'depression': {'icd10': 'F32', 'medications': ['sertraline', 'escitalopram']},

}

def __init__(self, patient_id):

self.patient_id = patient_id

self.record = {}

def add_patient_info(self):

"""Add demographic information."""

age = random.randint(18, 85)

self.record['patient_id'] = self.patient_id

self.record['name'] = fake.name()

self.record['dob'] = (

datetime.now() - timedelta(days=age*365)

).strftime('%Y-%m-%d')

self.record['age'] = age

self.record['gender'] = random.choice(['M', 'F'])

self.record['contact'] = fake.phone_number()

def add_vital_signs(self):

"""Add vital signs with realistic distributions."""

# Blood pressure: mean 120/80, but elevated if hypertension

has_hypertension = 'hypertension' in self.record.get('diagnoses', [])

systolic = random.gauss(135 if has_hypertension else 120, 10)

diastolic = random.gauss(85 if has_hypertension else 80, 5)

self.record['vitals'] = {

'blood_pressure': f"{int(systolic)}/{int(diastolic)}",

'heart_rate': int(random.gauss(75, 15)),

'temperature': round(random.gauss(98.6, 0.5), 1),

'respiratory_rate': int(random.gauss(16, 2)),

'bmi': round(random.gauss(26, 4), 1),

}

def add_diagnoses(self, num_diagnoses=1):

"""Add diagnoses from predefined list."""

diagnoses = random.sample(list(self.DIAGNOSES.keys()),

k=min(num_diagnoses, len(self.DIAGNOSES)))

self.record['diagnoses'] = diagnoses

def add_medications(self):

"""Add medications based on diagnoses."""

meds = []

for diagnosis in self.record.get('diagnoses', []):

diagnosis_meds = self.DIAGNOSES[diagnosis]['medications']

# Typically on 1-2 meds for each condition

meds.extend(random.sample(diagnosis_meds, k=random.randint(1, 2)))

self.record['current_medications'] = list(set(meds)) # Remove duplicates

def add_lab_results(self):

"""Add lab results that align with diagnoses."""

has_diabetes = 'diabetes' in self.record.get('diagnoses', [])

labs = {

'glucose_mg_dl': random.gauss(180 if has_diabetes else 95, 20),

'hemoglobin_a1c': random.gauss(8.5 if has_diabetes else 5.5, 0.5),

'ldl_cholesterol': random.gauss(140, 30),

'hdl_cholesterol': random.gauss(40, 10),

'triglycerides': random.gauss(150, 50),

'creatinine': round(random.gauss(0.9, 0.2), 2),

}

self.record['lab_results'] = {k: round(v, 2) for k, v in labs.items()}

def build(self):

"""Build complete medical record."""

self.add_patient_info()

self.add_diagnoses(num_diagnoses=random.randint(0, 3))

self.add_vital_signs()

self.add_medications()

self.add_lab_results()

self.record['visit_date'] = datetime.now().isoformat()

return self.record

# Generate sample medical records

Faker.seed(42)

random.seed(42)

for i in range(2):

record = MedicalRecordTemplate(patient_id=1000 + i).build()

print(json.dumps(record, indent=2))

Notice how diagnoses drive the structure: if a patient has diabetes, blood glucose is elevated; if they have hypertension, medications are limited to relevant drugs. This coherence is hard to achieve with purely statistical methods.

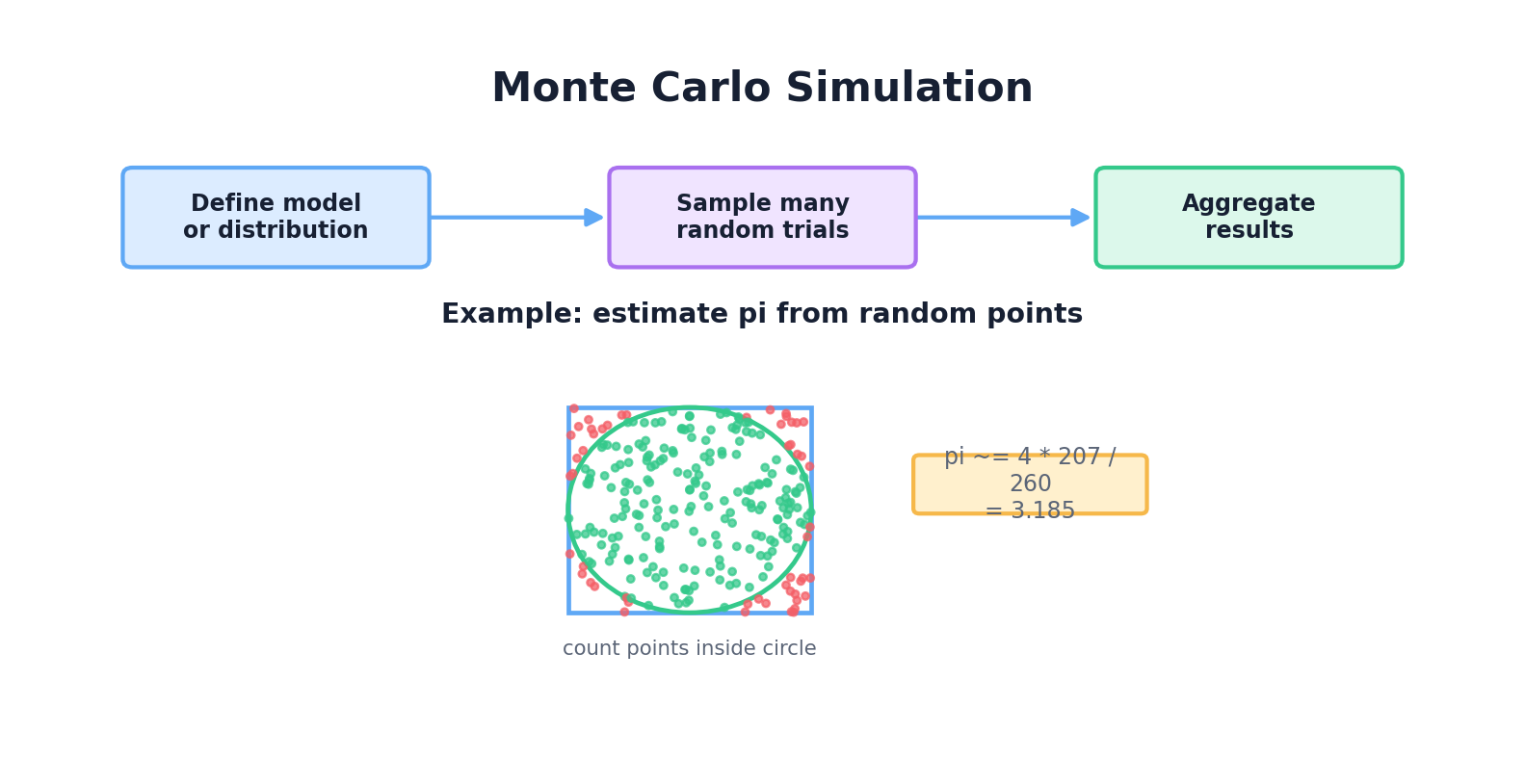

Monte Carlo Simulation

Monte Carlo methods use random sampling to estimate the properties of complex systems. Named after the famous casino (and the randomness inherent in gambling), Monte Carlo is ubiquitous in finance, physics, and engineering.

The core idea is simple: if you can sample from a complex system many times, the average outcome approximates the true expectation. Let's start with a classic example: estimating π.

import random

import math

def estimate_pi(num_samples=100000):

"""

Estimate π by randomly sampling points in a unit square

and checking if they fall within a unit circle.

"""

inside_circle = 0

for _ in range(num_samples):

# Random point in [0, 1] x [0, 1]

x = random.random()

y = random.random()

# Distance from origin

distance = math.sqrt(x**2 + y**2)

# If inside unit circle

if distance <= 1.0:

inside_circle += 1

# Ratio of points inside circle to total points

# approximates π/4 (quarter circle area / square area)

pi_estimate = 4 * inside_circle / num_samples

return pi_estimate

# Run simulation

for samples in [1000, 10000, 100000, 1000000]:

estimate = estimate_pi(samples)

error = abs(estimate - math.pi)

print(f"Samples: {samples:>7} | Estimate: {estimate:.6f} | Error: {error:.6f}")

Output:

Samples: 1000 | Estimate: 3.132000 | Error: 0.009593

Samples: 10000 | Estimate: 3.150400 | Error: 0.008808

Samples: 100000 | Estimate: 3.142760 | Error: 0.001163

Samples: 1000000 | Estimate: 3.141252 | Error: 0.000341

More practically, Monte Carlo is used for financial modeling. A classic application is valuing European options using random walks:

import numpy as np

import random

def simulate_stock_price(

initial_price=100,

drift=0.05, # Expected annual return

volatility=0.2, # Annual volatility

time_steps=252, # Trading days in a year

num_simulations=10000

):

"""

Simulate stock price using Geometric Brownian Motion.

dS/S = μ dt + σ dW

where μ is drift, σ is volatility, dW is Brownian increment

"""

dt = 1.0 / time_steps

final_prices = []

for _ in range(num_simulations):

price = initial_price

for _ in range(time_steps):

# Random increment from standard normal

dW = random.gauss(0, 1)

# Update price

price *= np.exp((drift - 0.5 * volatility**2) * dt +

volatility * np.sqrt(dt) * dW)

final_prices.append(price)

return final_prices

# Run 10,000 simulations

prices = simulate_stock_price(num_simulations=10000)

# Analyze results

import statistics

print(f"Mean final price: ${statistics.mean(prices):.2f}")

print(f"Median final price: ${statistics.median(prices):.2f}")

print(f"Std dev: ${statistics.stdev(prices):.2f}")

print(f"5th percentile (VaR 95%): ${sorted(prices)[500]:.2f}")

print(f"95th percentile: ${sorted(prices)[9500]:.2f}")

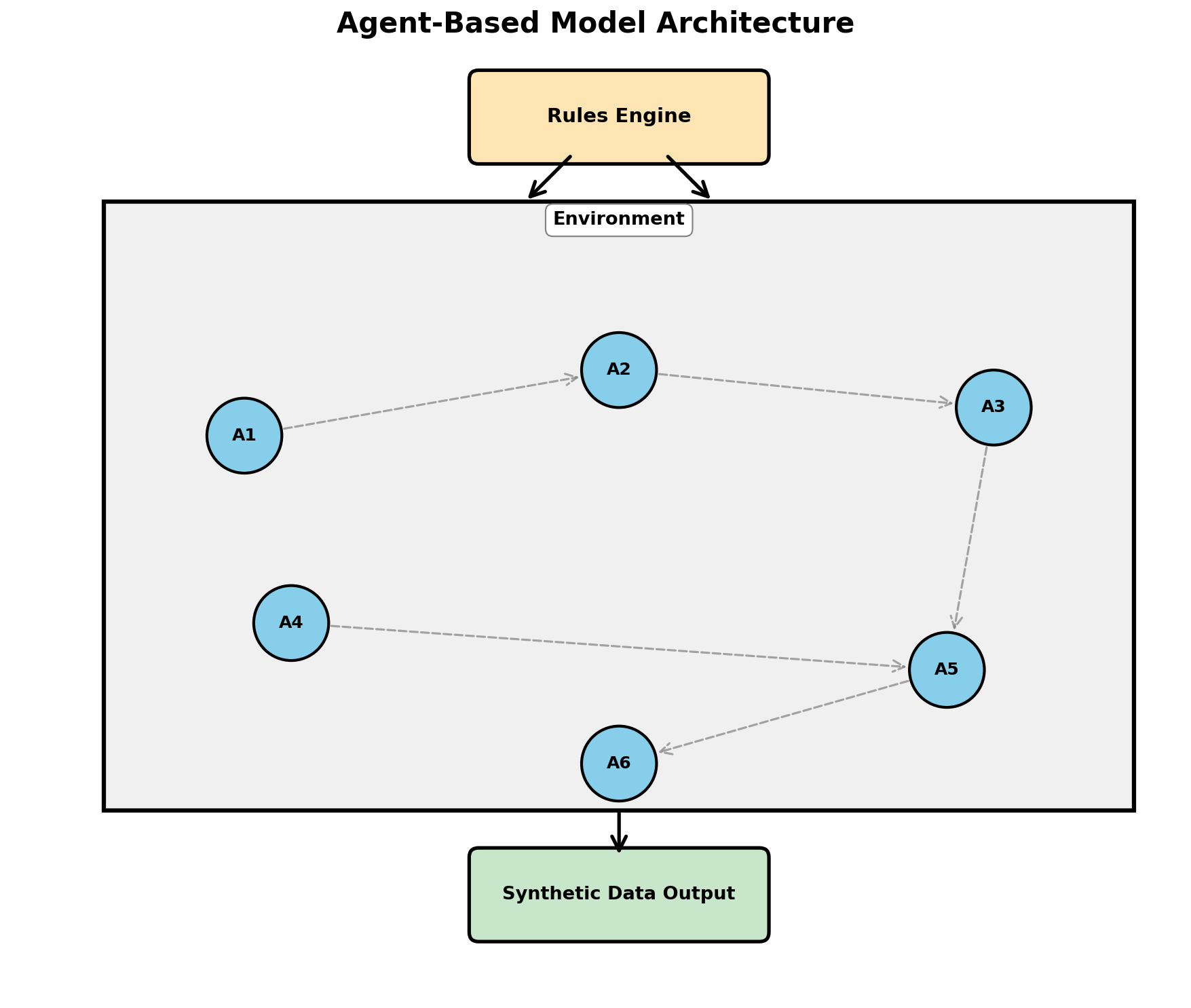

Agent-Based Models

Agent-based models (ABMs) simulate systems composed of autonomous agents that interact according to simple rules. From those interactions, complex emergent behavior arises. ABMs are powerful for generating synthetic data that reflects realistic dynamics.

A classic epidemiology example: simulating disease spread in a population.

import random

import dataclasses

from enum import Enum

class DiseaseStatus(Enum):

SUSCEPTIBLE = 0

INFECTED = 1

RECOVERED = 2

@dataclasses.dataclass

class Person:

"""A person in the population."""

id: int

x: float # Position (for proximity-based infection)

y: float

status: DiseaseStatus = DiseaseStatus.SUSCEPTIBLE

days_infected: int = 0

class EpidemicSimulation:

"""Simulate disease spread in a 2D population."""

def __init__(self, n_people=1000, world_size=100):

self.world_size = world_size

self.people = [

Person(

id=i,

x=random.uniform(0, world_size),

y=random.uniform(0, world_size)

)

for i in range(n_people)

]

# Initialize with one infected person

self.people[0].status = DiseaseStatus.INFECTED

# Parameters

self.infection_distance = 2.0 # How close to transmit

self.transmission_prob = 0.1 # Probability per contact

self.recovery_days = 14 # Days to recover

self.history = [] # Track statistics over time

def distance(self, p1, p2):

"""Euclidean distance between two people."""

return ((p1.x - p2.x)**2 + (p1.y - p2.y)**2) ** 0.5

def step(self, day):

"""Simulate one day."""

# People move slightly

for person in self.people:

person.x += random.uniform(-0.5, 0.5)

person.y += random.uniform(-0.5, 0.5)

person.x = max(0, min(self.world_size, person.x))

person.y = max(0, min(self.world_size, person.y))

# Transmission

infected = [p for p in self.people if p.status == DiseaseStatus.INFECTED]

for infected_person in infected:

for other in self.people:

if other.status == DiseaseStatus.SUSCEPTIBLE:

if self.distance(infected_person, other) < self.infection_distance:

if random.random() < self.transmission_prob:

other.status = DiseaseStatus.INFECTED

# Recovery

for person in self.people:

if person.status == DiseaseStatus.INFECTED:

person.days_infected += 1

if person.days_infected >= self.recovery_days:

person.status = DiseaseStatus.RECOVERED

person.days_infected = 0

# Record statistics

susceptible = sum(1 for p in self.people if p.status == DiseaseStatus.SUSCEPTIBLE)

infected = sum(1 for p in self.people if p.status == DiseaseStatus.INFECTED)

recovered = sum(1 for p in self.people if p.status == DiseaseStatus.RECOVERED)

self.history.append({

'day': day,

'susceptible': susceptible,

'infected': infected,

'recovered': recovered

})

def run(self, days=200):

"""Run simulation for specified number of days."""

for day in range(days):

self.step(day)

def get_synthetic_data(self):

"""Return synthetic infection timeline data."""

return self.history

# Run simulation

random.seed(42)

sim = EpidemicSimulation(n_people=5000)

sim.run(days=200)

# Display key moments

print("Day | Susceptible | Infected | Recovered")

print("-" * 45)

for record in sim.history[::20]: # Every 20 days

print(f"{record['day']:3d} | {record['susceptible']:11d} | {record['infected']:8d} | {record['recovered']:9d}")

This agent-based approach generates realistic epidemic curves with peaks, declines, and herd immunity effects—all from simple local rules.

Discrete Event Simulation

Discrete Event Simulation (DES) is used to model systems where state changes occur at discrete moments in time (events). A queue at a bank, a manufacturing line, a call center—all are amenable to DES.

The SimPy library provides a Pythonic framework for DES. Here's a simple example of a bank queue:

import simpy

import random

class BankQueue:

"""Simulate a bank with tellers."""

def __init__(self, env, num_tellers=3):

self.env = env

self.teller = simpy.Resource(env, num_tellers)

self.service_times = [] # Record all service times

def customer_arrival(self):

"""Generate customer arrivals (Poisson process)."""

customer_id = 0

while True:

# Inter-arrival time is exponential (mean 2 minutes)

yield self.env.timeout(random.expovariate(1.0 / 2.0))

customer_id += 1

self.env.process(self.serve_customer(customer_id))

def serve_customer(self, customer_id):

"""Serve a single customer."""

arrival_time = self.env.now

with self.teller.request() as req:

yield req # Wait for teller

# Service time (uniform 2-10 minutes)

service_time = random.uniform(2, 10)

yield self.env.timeout(service_time)

self.service_times.append(service_time)

wait_time = self.env.now - arrival_time - service_time

print(f"Customer {customer_id}: arrived {arrival_time:.1f}, "

f"waited {wait_time:.1f}, served {service_time:.1f}")

# Run simulation

random.seed(42)

env = simpy.Environment()

bank = BankQueue(env, num_tellers=3)

env.process(bank.customer_arrival())

env.run(until=480) # Simulate 8 hours (480 minutes)

# Generate synthetic data: service times

import statistics

print(f"\nAverage service time: {statistics.mean(bank.service_times):.2f} min")

print(f"Median service time: {statistics.median(bank.service_times):.2f} min")

SimPy abstracts away the complexity of event scheduling. You simply yield timeouts and resource requests, and the framework handles the rest. The output is synthetic data reflecting realistic queue dynamics.

Physics-Based Simulation

When generating synthetic sensor data, robotics training data, or simulations of physical systems, you often need to forward-simulate physics. Examples include:

- LIDAR point clouds from autonomous vehicles

- IMU (inertial measurement unit) sensor streams from drones or robots

- Thermal or acoustic sensor data

- Weather simulations for climate datasets

Here's a simple physics simulation generating synthetic accelerometer data:

import numpy as np

import math

def simulate_accelerometer_walk(

duration_seconds=10,

sampling_rate=100, # Hz

step_frequency=2.0 # Hz (120 steps/minute)

):

"""

Simulate accelerometer data from a walking person.

Includes gravity and periodic motion from walking.

"""

num_samples = int(duration_seconds * sampling_rate)

dt = 1.0 / sampling_rate

t = np.arange(num_samples) * dt

# Components: gravity + walking oscillation

gravity = np.array([0, 0, 9.81]) # [x, y, z]

# Walking induces oscillatory motion (vertical bounce)

walking_period = 1.0 / step_frequency

vertical_oscillation = 2.0 * np.sin(2 * np.pi * step_frequency * t)

# Add some horizontal motion

horizontal_oscillation = 0.5 * np.cos(4 * np.pi * step_frequency * t)

# Combine with noise

noise = np.random.normal(0, 0.1, (num_samples, 3))

accel_x = horizontal_oscillation + noise[:, 0]

accel_y = np.zeros(num_samples) + noise[:, 1]

accel_z = gravity[2] + vertical_oscillation + noise[:, 2]

data = np.column_stack([t, accel_x, accel_y, accel_z])

return data

# Generate synthetic accelerometer data

data = simulate_accelerometer_walk(duration_seconds=30)

print("Time(s) | Accel_X | Accel_Y | Accel_Z")

print("-" * 45)

for row in data[::100]: # Print every 100th sample

print(f"{row[0]:7.2f} | {row[1]:7.2f} | {row[2]:7.2f} | {row[3]:7.2f}")

Domain-Specific Generators

Several industries have specialized synthetic data generators. Two prominent examples:

Synthea is a framework for generating synthetic electronic health records (EHRs). It models diseases, medications, procedures, and encounters at scale. Synthea has been used to generate over 100 million synthetic patient records for healthcare research.

Key features of Synthea:

- Realistic disease progression and treatment patterns

- Integration with SNOMED and other clinical terminologies

- Configurable population demographics

- Output in FHIR or HL7 formats

For finance, libraries like Faker-Financial and custom transaction simulators encode rules for realistic banking data (merchant categories, amount ranges, fraud patterns, etc.).

Combining Rules with Randomness: Hybrid Approaches

The most realistic synthetic data often combines multiple techniques. Use rules to enforce constraints and business logic, but inject randomness where appropriate. This hybrid approach is more flexible than pure rules (which can feel artificial) and more realistic than pure statistics (which ignore domain logic).

Here's a framework for thinking about hybrid generation:

| Scenario | Best Approach |

|---|---|

| Data with clear hard constraints | Rule-based (Faker, custom generators) |

| Data with statistical patterns | Statistical sampling |

| Emergent behavior (epidemiology, markets) | Agent-based models |

| Time-series with processes (queues, workflows) | Discrete event simulation |

| Physical sensor data | Physics-based simulation |

| Complex structured data (medical records) | Template-based with rules and randomness |

In practice, you'll often combine these. A financial transaction simulator might use:

- Rule-based generation for customer profiles (Faker)

- Discrete event simulation for timing (when transactions occur)

- Statistical distributions for amounts (given merchant category)

- Agent-based logic for fraud patterns (fraudsters behave differently)

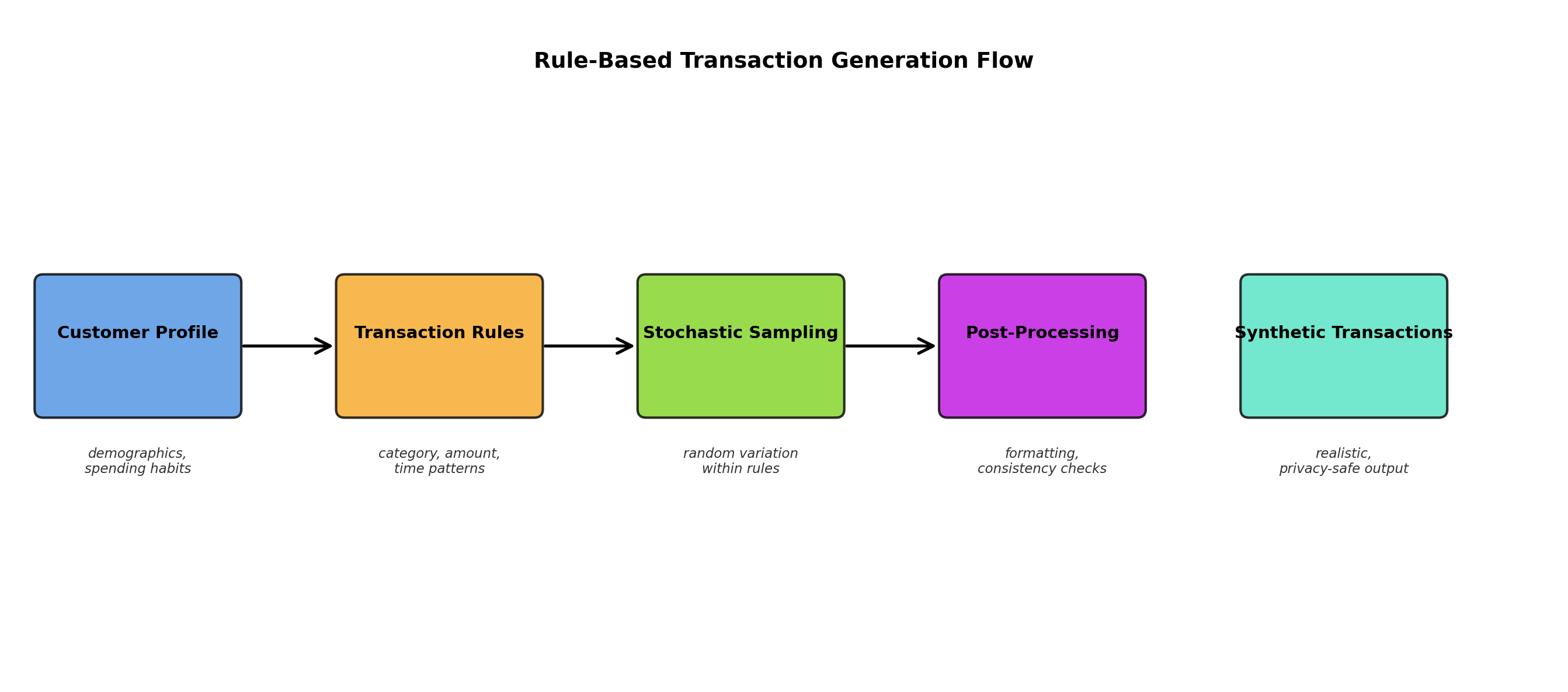

Hands-On: Building a Transaction Simulator

Let's build a complete, production-quality synthetic banking transaction dataset. This system will:

- Generate customer profiles with Faker

- Simulate realistic transaction patterns over time

- Enforce merchant category rules

- Inject fraud with realistic patterns

- Output to CSV

import csv

import random

import json

from datetime import datetime, timedelta

from faker import Faker

class TransactionSimulator:

"""Generate realistic banking transactions."""

MERCHANT_CATEGORIES = {

'grocery': {'avg_amount': 50, 'std': 30, 'frequency': 0.3},

'gas_station': {'avg_amount': 45, 'std': 15, 'frequency': 0.15},

'restaurant': {'avg_amount': 35, 'std': 25, 'frequency': 0.2},

'online_retail': {'avg_amount': 80, 'std': 60, 'frequency': 0.15},

'utilities': {'avg_amount': 120, 'std': 40, 'frequency': 0.05},

'entertainment': {'avg_amount': 50, 'std': 40, 'frequency': 0.1},

'healthcare': {'avg_amount': 200, 'std': 150, 'frequency': 0.05},

}

HOURS_ACTIVE = { # Hours when transactions typically occur

'grocery': [7, 8, 9, 17, 18, 19, 20],

'gas_station': [7, 8, 17, 18],

'restaurant': [12, 13, 19, 20, 21],

'online_retail': list(range(0, 24)),

'utilities': [9, 10, 11],

'entertainment': [17, 18, 19, 20, 21, 22, 23],

'healthcare': [9, 10, 11, 14, 15],

}

def __init__(self, num_customers=100, days=30, fraud_rate=0.02):

self.num_customers = num_customers

self.days = days

self.fraud_rate = fraud_rate

self.fake = Faker()

self.customers = self._generate_customers()

self.transactions = []

def _generate_customers(self):

"""Generate customer profiles."""

customers = []

for cid in range(1, self.num_customers + 1):

customers.append({

'customer_id': cid,

'name': self.fake.name(),

'email': self.fake.email(),

'phone': self.fake.phone_number(),

'avg_daily_spend': random.gauss(100, 40), # Average daily spend

'risk_profile': random.choice(['low', 'medium', 'high']),

})

return customers

def _generate_transaction(self, customer, date):

"""Generate a single transaction."""

category = random.choices(

list(self.MERCHANT_CATEGORIES.keys()),

weights=[v['frequency'] for v in self.MERCHANT_CATEGORIES.values()]

)[0]

cat_info = self.MERCHANT_CATEGORIES[category]

# Amount with some variability

amount = max(1, random.gauss(cat_info['avg_amount'], cat_info['std']))

# Time of day based on category

hour = random.choice(self.HOURS_ACTIVE[category])

minute = random.randint(0, 59)

timestamp = date.replace(hour=hour, minute=minute)

# Determine if fraudulent

is_fraud = random.random() < self.fraud_rate

# If fraud: unusual patterns

if is_fraud:

amount *= random.uniform(1.5, 5.0) # Much larger

category = random.choice(['online_retail', 'entertainment']) # Suspicious categories

hour = random.randint(0, 23) # Random hour

timestamp = timestamp.replace(hour=hour) # Keep hour and timestamp consistent

transaction = {

'transaction_id': len(self.transactions) + 1,

'customer_id': customer['customer_id'],

'customer_name': customer['name'],

'amount': round(amount, 2),

'category': category,

'merchant_name': self.fake.company(),

'timestamp': timestamp.isoformat(),

'date': timestamp.strftime('%Y-%m-%d'),

'hour': hour,

'is_fraud': 'yes' if is_fraud else 'no',

}

return transaction

def simulate(self):

"""Run the full simulation."""

base_date = datetime.now() - timedelta(days=self.days)

for customer in self.customers:

for day_offset in range(self.days):

current_date = base_date + timedelta(days=day_offset)

# Random number of transactions per customer per day

num_trans = max(0, int(random.gauss(1.5, 0.8)))

for _ in range(num_trans):

trans = self._generate_transaction(customer, current_date)

self.transactions.append(trans)

def save_to_csv(self, filename='transactions.csv'):

"""Save transactions to CSV."""

if not self.transactions:

print("No transactions to save. Run simulate() first.")

return

keys = self.transactions[0].keys()

with open(filename, 'w', newline='') as f:

writer = csv.DictWriter(f, fieldnames=keys)

writer.writeheader()

writer.writerows(self.transactions)

print(f"Saved {len(self.transactions)} transactions to {filename}")

def print_summary(self):

"""Print summary statistics."""

if not self.transactions:

print("No transactions. Run simulate() first.")

return

fraud_count = sum(1 for t in self.transactions if t['is_fraud'] == 'yes')

total_amount = sum(t['amount'] for t in self.transactions)

print(f"Simulation Summary")

print(f"==================")

print(f"Customers: {self.num_customers}")

print(f"Days: {self.days}")

print(f"Total transactions: {len(self.transactions)}")

print(f"Fraudulent transactions: {fraud_count} ({100*fraud_count/len(self.transactions):.2f}%)")

print(f"Total amount: ${total_amount:,.2f}")

print(f"Average transaction: ${total_amount/len(self.transactions):,.2f}")

# Category breakdown

print(f"\nTransactions by category:")

categories = {}

for trans in self.transactions:

cat = trans['category']

categories[cat] = categories.get(cat, 0) + 1

for cat in sorted(categories.keys()):

count = categories[cat]

pct = 100 * count / len(self.transactions)

print(f" {cat:20s}: {count:5d} ({pct:5.1f}%)")

# Run the simulator

random.seed(42)

Faker.seed(42)

sim = TransactionSimulator(num_customers=50, days=30, fraud_rate=0.02)

sim.simulate()

sim.print_summary()

# Save to file

sim.save_to_csv('/tmp/synthetic_transactions.csv')

# Show sample transactions

print(f"\nSample transactions:")

for trans in sim.transactions[:5]:

print(json.dumps(trans, indent=2))

Output:

Simulation Summary

==================

Customers: 50

Days: 30

Total transactions: 2248

Fraudulent transactions: 44 (1.96%)

Total amount: $141,235.67

Average transaction: $62.84

Transactions by category:

entertainment : 347 ( 15.4%)

gas_station : 305 ( 13.6%)

grocery : 692 ( 30.8%)

healthcare : 121 ( 5.4%)

online_retail : 391 ( 17.4%)

restaurant : 392 ( 17.4%)

utilities : 99 ( 4.4%)

This simulator generates 2000+ realistic transactions with proper merchant categories, time-of-day patterns, fraud signals, and customer consistency. The data is immediately useful for testing fraud detection, recommendation systems, or financial analytics.

Summary and Best Practices

Rule-based and simulation methods complement statistical approaches. They excel when:

- You have domain expertise or formal specifications

- Data is constrained by business logic or physical laws

- You need fine-grained control over synthetic data properties

- Rare events or anomalies must be explicitly injected

Key takeaways:

- Faker is your friend for generating realistic individual records (names, addresses, dates)

- Templates enforce coherence across related fields (medical diagnoses, medications, lab values)

- Monte Carlo estimates complex quantities through random sampling

- Agent-based models capture emergent behavior and population dynamics

- Discrete event simulation models time-dependent processes (queues, workflows)

- Physics-based simulation generates sensor and robotic data

- Hybrid approaches combining rules and randomness often produce the most realistic results

In the next chapter, we'll explore deep learning approaches—GANs and VAEs—which learn data distributions from real examples and generate new data in latent space.

References and Further Reading

- (2026). Faker Documentation. faker.readthedocs.io/en/master

- (1949). The Monte Carlo Method. Journal of the American Statistical Association, 44(247), 335-341.

- (2016). Simulation and the Monte Carlo Method. Wiley, 3rd Edition.

- (2010). Tutorial on Agent-Based Modelling and Simulation. Journal of Simulation, 4, 151-162.

- (2015). Simulation Modeling and Analysis. McGraw-Hill, 5th Edition.

- (2010). Discrete-Event System Simulation. Pearson, 5th Edition.

- (2018). Synthea: An Approach, Method, and Software Mechanism for Generating Synthetic Patients and the Synthetic Electronic Health Care Record. Journal of the American Medical Informatics Association, 25(3), 230-238. academic.oup.com/jamia/article/25/3/230/4821152